How to Build a Pitch Deck Investors Actually Read

Founders build pitch decks as if investors were going to study them. They won't.

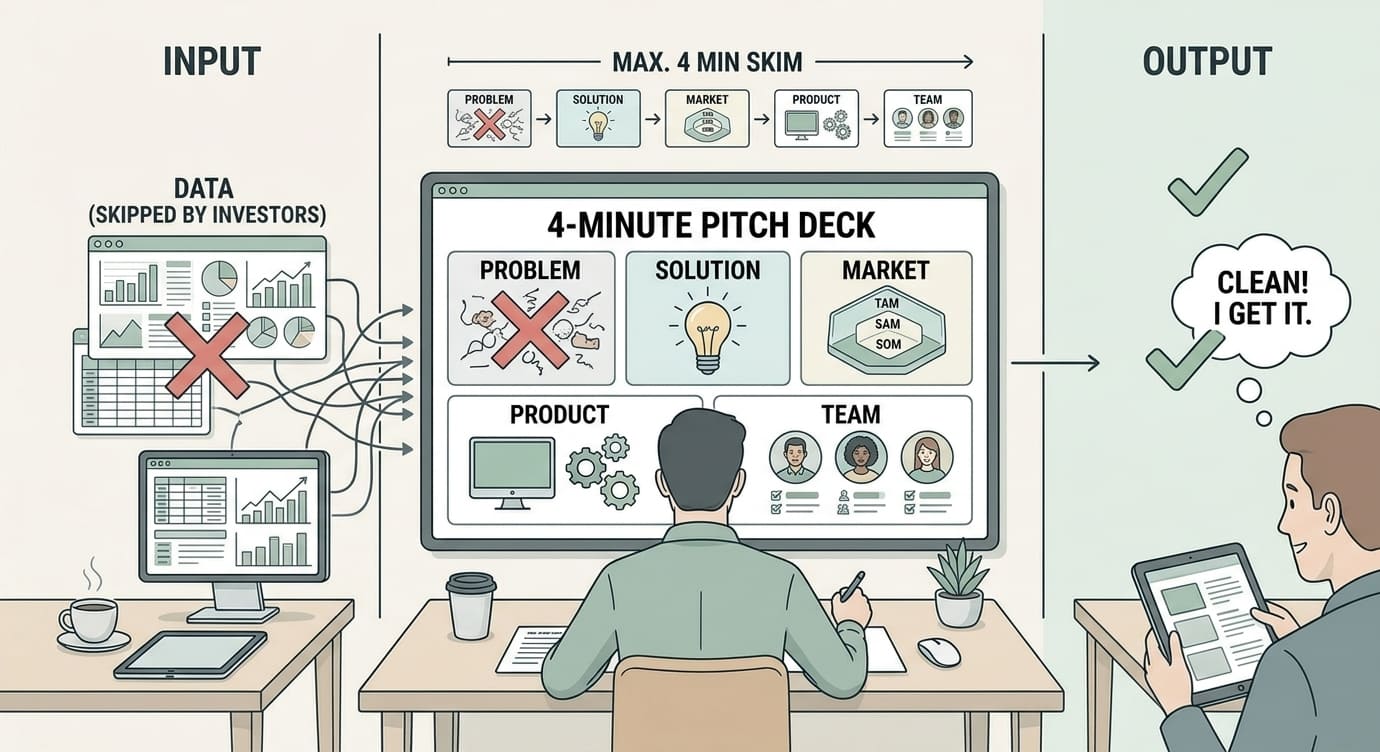

According to DocSend's own research on seed decks, VCs spend an average of three minutes and 44 seconds reviewing a seed pitch deck. That is the entire window. Not per meeting — per deck. Every slide you add, every paragraph of text, every clever-but-unclear headline is competing for a share of those four minutes.

Once you accept that number, most pitch deck advice simplifies itself. The deck is not a document that explains your business. It is a filter that decides whether a conversation about your business happens at all.

This piece breaks down what a seed deck is actually for, what each slide has to accomplish, the mistakes that end the read early, and a test you can run before sending it to anyone.

The Deck Has One Job

A common mistake is treating the pitch deck like a compressed business plan — a place to prove everything: the market, the model, the roadmap, the vision, the defensibility, all of it.

That framing produces 25-slide decks that answer questions nobody asked yet and bury the one question every early-stage investor is actually asking: is this worth a meeting?

That is the whole job. The deck earns a conversation. The conversation earns diligence. Diligence earns the check. Each stage has its own materials, and the deck only has to win the first one.

This is liberating in practice. You do not need to resolve every objection inside the deck. You need to make the opportunity legible fast, show evidence that you are the ones to pursue it, and leave enough genuine substance that the investor's next thought is "I want to ask them about this" rather than "I don't get it."

It also explains why the strongest reference materials for seed decks are so plain. Y Combinator's seed deck template is deliberately spare — a small number of simple slides, each carrying one idea. That plainness is not a lack of effort. It is the format that survives a fast read.

Design for the Skim, Not the Study

Under four minutes across a full deck means seconds per slide. A few consequences follow directly.

One idea per slide. If a slide needs a paragraph of explanation, it is two slides — or the idea isn't clear yet. The headline of each slide should carry the point on its own, so that someone reading only the headlines still gets the story.

Legible from a distance. Guy Kawasaki's well-known 10/20/30 rule — ten slides, twenty minutes, no font smaller than 30 points — was written for live pitches, but the font rule encodes something deeper: if you need small text to fit your content, you have too much content. His sharper point is worth sitting with: if you need more than ten slides to explain the business, the problem is usually the business's clarity, not the slide count.

Front-load the story. An investor who is not hooked by slide four rarely recovers interest by slide fourteen. DocSend's guidance makes the same point from data: slide order matters, and decks that open with the core narrative — purpose, problem, solution — perform better than decks that warm up slowly.

Numbers over adjectives. "Growing fast" is decoration. "From 40 to 210 paying users in four months" is information. In a skim, concrete numbers are gravity — they are where the eye stops.

What Each Slide Has to Do

Slide lists vary between templates, but the underlying questions barely change. Here is the core set, with the job each one has to do.

Title: what is this, in one sentence?

Company name plus a one-line description a stranger would understand. Plain beats clever. If a smart person outside your industry cannot repeat back what you do after reading this slide, rewrite it until they can.

Problem: why does this matter?

Describe the problem concretely, from the customer's side, ideally with a number or a real scenario attached. The trap here is abstraction — "small businesses struggle with marketing" describes nothing. Whose problem, in what moment, costing what?

If you have done real validation work, this slide is where it pays off. Founders who have talked to actual customers write problem slides in the customer's language; founders who haven't write in category language. Investors can tell the difference in seconds. If your problem evidence is still thin, that gap is worth closing before you pitch — we've written before about what real validation looks like.

Solution: what do you do about it?

What the product does, stated simply, connected directly to the problem you just described. Show the product if you can — a screenshot or a before/after beats a paragraph of description. Resist listing features. One clear mechanism, explained well, is stronger than six capabilities in bullet form.

Traction: what proof exists?

This is often the most-read slide in the deck, and it deserves honesty. Revenue, paying users, retention, growth rate — with timeframes, because momentum is the story, not the raw number.

If you are pre-revenue, do not fake gravity with vanity metrics. Show what you genuinely have: waitlist signups with real intent, pilot commitments, usage from an early cohort, or the speed at which you've shipped. Early-stage investors calibrate for stage. What they are reading for is evidence of movement and honesty about where you are.

Market: is this big enough to matter?

Investors want to see that the opportunity can support a real company, and they want to see that you did the thinking yourself. A bottom-up estimate — how many target customers, at what realistic price — is far more credible than a giant top-down number lifted from an industry report. We've covered the full method in our guide to estimating market size; the deck version is one slide with transparent math.

Business model: how does money flow?

How you charge, what you charge, and roughly what a customer is worth. At seed stage nobody expects a perfected model. They expect you to have a clear, defensible starting hypothesis and to know your own numbers.

Competition: who else, and why you?

Never claim you have no competitors — the alternative might be a spreadsheet or doing nothing, but it exists, and pretending otherwise reads as naivety. The stronger move is to name the real alternatives and state plainly what you do differently and for whom. Positioning, not dismissal.

Team: why you, specifically?

Concrete accomplishments and relevant unfair advantages — domain years, technical depth, distribution access, previous builds. Titles and logos matter less than a specific reason to believe this team wins this market. Solo founders: address it head-on rather than hoping nobody notices. How you work, how you've shipped, and what you've already built alone can be an argument in your favor.

The ask: what do you need, for what?

A specific amount and what it buys in milestones. DocSend's current guidance notes that showing 18 to 24 months of runway is the standard investors now expect, along with the milestones that raise makes possible. A vague ask ("we're raising to accelerate growth") signals that the plan behind it is equally vague.

The Mistakes That End the Read Early

A handful of failures show up so consistently that they are worth naming as a checklist of their own.

Jargon in the first three slides. Every acronym and insider term is a small tax on the reader's attention, and the budget is four minutes. Write the opening slides so a smart outsider follows effortlessly.

Text walls. A slide the investor has to read rather than see breaks the skim. If a slide looks like a document, it will be treated like one — skipped.

The unexplained hockey stick. Projections that leap from zero to millions with no visible assumptions damage credibility rather than building it. If you show projections at all, show the logic under them.

Hidden weaknesses that surface anyway. A crowded market, a single-founder team, a platform dependency — investors will spot these within minutes whether you mention them or not. Naming a weakness and showing how you think about it converts a red flag into evidence of judgment.

A deck that needs you standing next to it. Most seed decks are read cold, forwarded in emails, skimmed on phones. If the story only works with your narration, it does not work.

The Test Before You Send It

Before your deck goes to a single investor, run it through three cheap checks.

The four-minute test. Give the deck to someone smart who knows nothing about your company. Take it away after four minutes. Ask them: What does the company do? Who is it for? Why would it win? Every wrong or missing answer maps to a specific slide that needs work.

The headline test. Read only the slide headlines, top to bottom. Do they tell the complete story on their own? If not, rewrite headlines until they do — the body of each slide is supporting evidence, not the narrative.

The skeptic test. Ask someone to read it looking for reasons to say no, and to say them out loud. You will hear the objections investors will think but rarely tell you. You do not have to answer all of them inside the deck — but you should know which ones you are choosing to leave for the meeting.

Then expect to revise between conversations. A deck is not a one-time artifact; every pitch that generates confused questions is telling you which slide failed.

Clarity Is the Strategy

There is no slide trick that makes a weak business fundable, and a mediocre deck can still get a strong business meetings if it reaches the right people. The deck is not the company.

But within its real job — earning the conversation — clarity is nearly everything. The founders who do well in those four minutes are not the ones with the most polished design or the biggest market number. They are the ones whose deck a tired investor can skim at 11 p.m. and still walk away able to repeat what the company does, why now, and why this team.

Build for that reader. Everything else is decoration.

If you're preparing your pitch, VynaroAI's pitch deck and investor script tools help you build the narrative from your actual business context — problem, market, positioning, and ask — instead of a blank template. Start at VynaroAI.